Selling your home FSBO means you’re in control of the process—but it also means you’re tackling all the details, including taxes. And when it comes to closing costs, you might be wondering: Can I deduct any of these expenses come tax season?

The short answer? Some, but not all. The IRS has specific rules about what’s deductible and what isn’t; understanding them can help you keep more money in your pocket. In this guide, we’ll break down which closing costs might offer you a tax advantage and how to ensure you’re not leaving any savings on the table.

Let’s dive in and make sense of the tax implications of your home sale—so you can maximize your profits and minimize your tax bill!

What are Closing Costs?

Closing costs are the various fees and expenses that come with finalizing the sale of a home. As an FSBO seller, you won’t have to pay a listing agent’s commission, but you’ll still face certain costs before handing over the keys.

These expenses typically include:

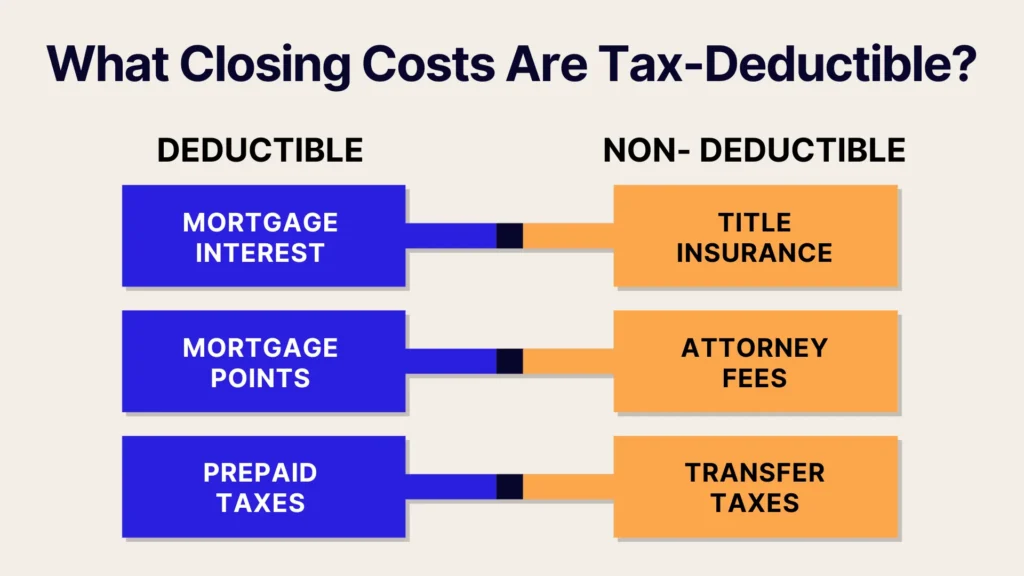

- Title search and title insurance: Ensures the buyer gets a clear title.

- Attorney fees: If required in your state, an attorney will handle legal paperwork.

- Transfer taxes: Some local governments charge a tax when property ownership changes hands.

- Recording fees: Covers the cost of updating public land records.

- Prorated property taxes: You may need to cover property taxes until the sale date.

While some of these costs are unavoidable, others may be negotiable. Understanding what you’re responsible for helps you budget effectively and determine if any expenses might be tax-deductible.

Can Closing Costs Be Tax-Deductible?

As an FSBO seller, you're likely looking for ways to reduce your tax burden after selling your home. While most closing costs aren’t directly tax-deductible, certain expenses related to mortgage interest and property taxes may qualify. The IRS allows deductions for specific expenses considered part of homeownership rather than the transaction itself.

To determine what you can deduct, you must review your HUD-1 Settlement Statement or Closing Disclosure, which outlines all fees paid at closing. Below, we’ll cover two key deductions that could apply to you: mortgage interest payments and real estate property taxes.

Mortgage Interest Payments

If you're still paying off a mortgage when you sell, any interest you pay as part of the closing process may be deductible. This typically includes:

- Prepaid mortgage interest (also known as “per diem”): If you sold your home mid-month, you might owe interest for the month before your loan is fully paid. This interest is usually deductible.

- Mortgage points: If you originally paid discount points to lower your interest rate when you bought the home, you can deduct any remaining unused points when you sell.

These deductions are reported on IRS Form 1098, which your lender will provide. Remember that different tax rules may apply if your home is used for business or rental purposes.

Real Estate Property Taxes

Property taxes paid at closing may be deductible as part of your overall real estate tax deductions. If you prepaid property taxes for the year and the buyer reimbursed you at closing, you can only deduct the portion you paid.

On the other hand, if you owed unpaid property taxes at the time of sale, the amount you pay at closing is deductible. These taxes are typically listed on your closing statement and can be claimed as an itemized deduction on Schedule A (Form 1040).

Understanding which closing costs qualify for deductions can help FSBO sellers maximize their tax savings. Always consult a tax professional to ensure you take full advantage of potential deductions while complying with IRS rules.

Points or Loan Origination Fees

If you paid points or loan origination fees when you took out your mortgage, you can deduct them when selling your home. Points, also known as prepaid interest, can either be deducted in full in the year they were paid or spread out over the life of the loan (amortized).

When you sell your home, any remaining undeducted points may be claimed as a deduction in that tax year. However, the IRS has specific rules, so it’s best to check IRS Form 1098 and consult a tax professional to ensure you claim the deduction correctly.

How to Claim Closing Cost Deductions

To take advantage of tax-deductible closing costs, you must itemize your deductions rather than take the standard deduction. This means listing eligible expenses on Schedule A (Form 1040) when filing your taxes. While itemizing takes more effort, it can lead to greater tax savings if your deductions exceed the standard deduction amount.

Itemizing Deductions on Schedule A

When filing your tax return, follow these steps to claim deductible closing costs:

- Gather Your Closing Documents

- Review your Closing Disclosure or HUD-1 Settlement Statement to identify deductible expenses, such as mortgage interest, points, and property taxes.

- Obtain IRS Form 1098 from your lender, which reports mortgage interest paid.

- Determine Your Deductible Expenses

- Mortgage interest payments: Reported on Line 8a of Schedule A.

- Mortgage points: If deductible, report them on Line 8d under "Points Not Reported on Form 1098."

- Property taxes paid at closing: Listed on Line 5b under “State and Local Real Estate Taxes.”

- Compare With the Standard Deduction

- For 2024, the standard deduction is $14,600 for single filers and $29,200 for married couples filing jointly (these amounts may change yearly).

- If your total itemized deductions exceed this amount, itemizing will likely provide more significant tax benefits.

- File Schedule A With Your Tax Return

- Attach Schedule A to your Form 1040 when submitting your tax return.

- Keep all supporting documents in case of an IRS audit.

If you’re unsure whether itemizing is the best choice, consult a tax professional to ensure you maximize your deductions while staying compliant with IRS rules.

Limitations on Deducting Closing Costs

While certain closing costs may be tax-deductible, there are limitations on how much you can deduct and under what circumstances. The IRS has strict rules regarding mortgage interest deductions, property tax deductions, and eligibility criteria based on the purpose of the home. Below, we cover two key limitations that FSBO sellers should be aware of: loan amount limits and the requirement that the property must be a primary residence for the buyer.

Loan Amount Limits up to $750,000

The IRS sets a cap on how much mortgage interest can be deducted based on the total loan amount. As of 2024, the following limits apply:

- Loans taken out after December 15, 2017: You can deduct interest on mortgage debt up to $750,000 (or $375,000 for married individuals filing separately).

- Loans taken out before December 15, 2017: The higher limit of $1 million (or $500,000 for married filing separately) still applies.

This means that if the buyer of your home takes out a mortgage exceeding these limits, they will only be able to deduct interest on the portion of the loan that falls within the threshold. As a FSBO seller, this doesn't directly impact your tax return, but it's useful to understand how your buyer's financial situation may influence negotiations, particularly if they are close to these deduction limits.

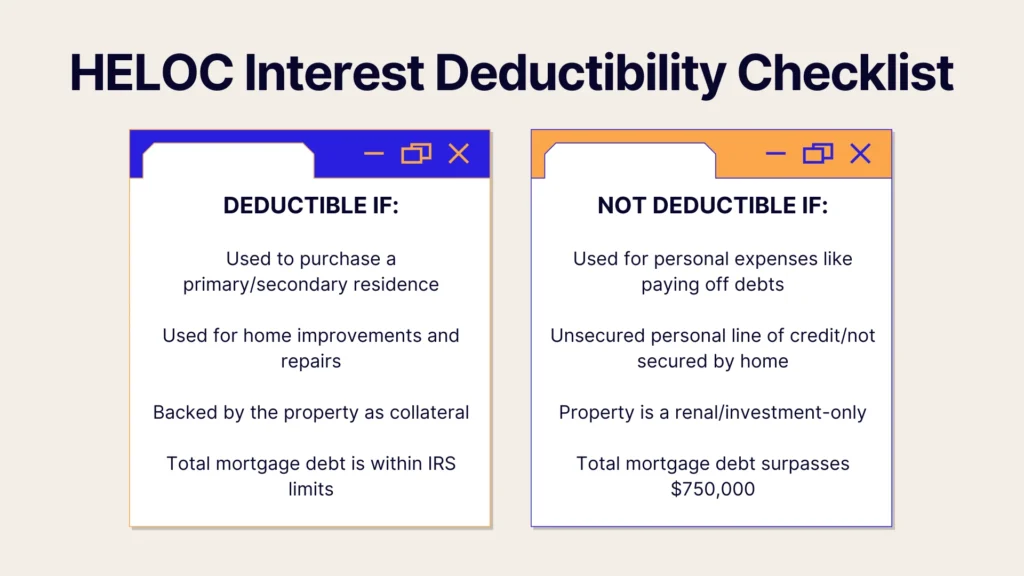

Additionally, home equity loans or lines of credit (HELOCs) are only deductible if they were used to buy, build, or substantially improve the home. If a buyer finances part of their purchase with a HELOC not used for home improvements, they may not be able to deduct the interest.

Must Be for the Buyer’s Primary Residence

For mortgage interest and points to be tax-deductible, the home must be used as the buyer’s primary residence. This means:

- The home must be where the buyer lives most of the time during the year.

- Second homes and investment properties do not qualify for the same deductions.

- The buyer must have a mortgage secured by the property—cash purchases do not qualify for mortgage interest deductions.

As a FSBO seller, this may impact negotiations if your potential buyers are purchasing an investment property, as they won’t benefit from certain deductions. If your home is attractive to investors, understanding these limitations can help you set realistic expectations and adjust your selling strategy accordingly.

Specific Closing Costs That are Deductible

While most closing costs aren’t tax-deductible, some expenses qualify under specific IRS rules. Two key deductions available to certain taxpayers are mortgage insurance premiums and prepaid mortgage interest. Understanding these deductions can help you or your buyer maximize tax savings.

Mortgage Insurance Premiums for Some Taxpayers

Mortgage insurance premiums (MIP) can be deductible if your mortgage was issued after 2006 and meets income requirements. This applies to:

- Private Mortgage Insurance (PMI): Typically required for conventional loans with a down payment of less than 20%.

- FHA Mortgage Insurance Premiums: Required for FHA loans.

- VA and USDA Loan Fees: While not labeled as "mortgage insurance," the VA funding fee and USDA guarantee fee may also be deductible.

However, there are income limits:

- The deduction begins to phase out at an adjusted gross income (AGI) of $100,000 for single and joint filers ($50,000 for married filing separately).

- The deduction is eliminated once AGI reaches $109,000 ($54,500 for married filing separately).

If eligible, you can deduct MIP on Schedule A (Form 1040) under mortgage interest.

Prepaid Interest Under Mortgage Interest Deduction

Prepaid interest, also called per diem interest, is the amount paid upfront to cover interest between the closing date and the start of the first mortgage payment. This is common when a home closes mid-month.

- Prepaid interest is fully deductible in the year it is paid.

- It will appear on your Closing Disclosure and IRS Form 1098, provided by your lender.

To claim this deduction, report the amount on Schedule A, Line 8a under "Home Mortgage Interest and Points." This helps reduce taxable income, making it a valuable deduction for homeowners.

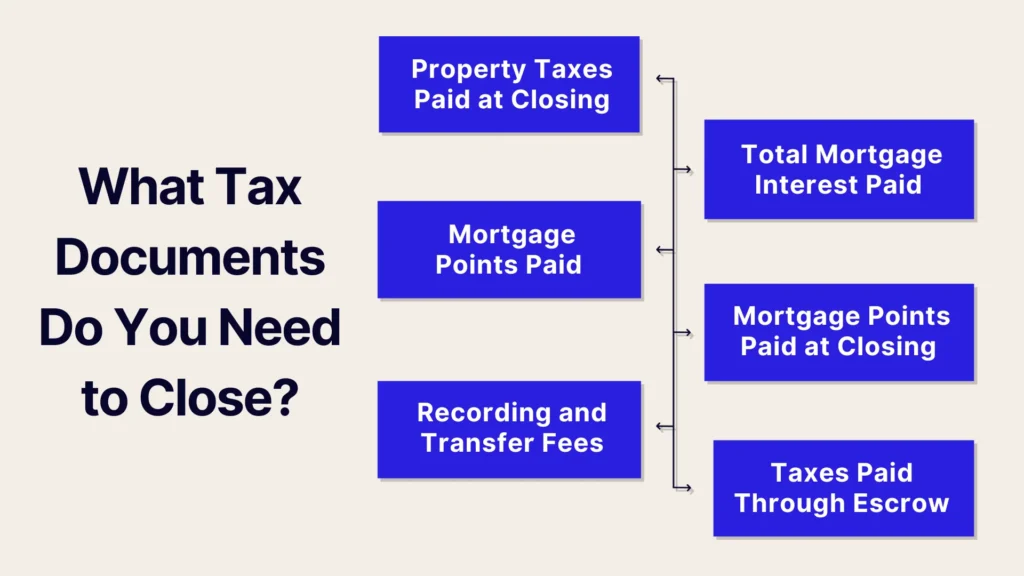

Records and Documentation Needed

To claim any tax deductions related to closing costs, accurate record-keeping is essential. The IRS requires documentation to verify deductible expenses, and having the right paperwork will ensure you maximize your tax benefits while staying compliant. Two key documents you’ll need are the HUD-1 Settlement Statement and Form 1098.

HUD-1 Settlement Statement for Closing Costs

If you sold your home before October 2015, you likely received a HUD-1 Settlement Statement, which provides a detailed breakdown of all closing costs. While FSBO sellers today typically receive a Closing Disclosure instead, the HUD-1 remains valid for tax purposes if applicable.

- The HUD-1 or Closing Disclosure lists all fees paid at closing, including property taxes, mortgage points, and prepaid interest, which may be deductible.

- If you paid real estate property taxes at closing, they will be itemized on this statement.

- Keep this document for at least three years after filing your tax return in case of an IRS audit.

If your transaction used a Closing Disclosure instead of a HUD-1, it serves the same purpose for tax deductions.

Form 1098 for Mortgage Interest Deduction

Your mortgage lender will provide IRS Form 1098 if you paid over $600 in mortgage interest during the tax year. This form details:

- Total mortgage interest paid, which may be deductible.

- Points paid at closing, if applicable.

- Prepaid interest, which should match the amount listed on your Closing Disclosure.

To claim deductions, report the amounts from Form 1098 on Schedule A (Form 1040) under mortgage interest. Compare Form 1098 with your closing statement to ensure accuracy, and keep copies of both in your records for tax reporting.

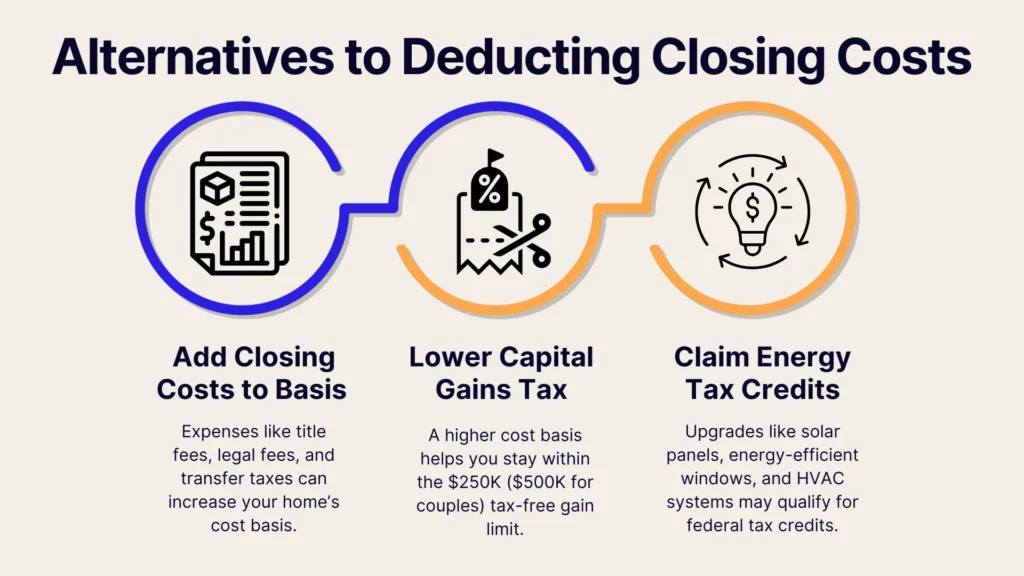

Alternatives to Deducting Closing Costs

If you’re unable to deduct certain closing costs on your tax return, there are still ways to gain tax benefits from these expenses. Two key alternatives include adding closing costs to your home’s tax basis and claiming tax credits for energy-efficient improvements. These strategies can help reduce your capital gains tax liability when you sell or provide immediate tax savings if you've made eligible home upgrades.

Adding Closing Costs to Home's Tax Basis

Some closing costs can’t be deducted, but they can be added to your home’s cost basis, which helps reduce your taxable capital gains when you sell. The cost basis is the original purchase price of your home, plus eligible expenses that increase its value.

- Eligible costs to add to basis include:

- Title fees

- Legal fees for the purchase

- Transfer taxes

- Surveys and recording fees

By increasing your home’s cost basis, you reduce the profit (capital gains) you must report when selling, which can help you stay within the $250,000 ($500,000 for married couples) capital gains exclusion limit.

Deductions for Energy-Efficient Home Improvements

If you made energy-efficient upgrades at the time of purchase, you may qualify for federal tax credits. Eligible improvements include:

- Solar panels or solar water heaters (Federal Solar Investment Tax Credit)

- Energy-efficient windows, doors, and insulation

- High-efficiency HVAC systems or water heaters

These upgrades may qualify for residential energy credits on Form 5695. Unlike deductions, tax credits provide a dollar-for-dollar reduction of your tax bill, making them a valuable way to offset costs associated with homeownership.

Impact of Tax Law Changes on Deductions

Tax laws affecting homeownership deductions have changed in recent years, particularly with the Tax Cuts and Jobs Act (TCJA) of 2017. These changes impact how much mortgage interest and property taxes homeowners can deduct, which may affect the financial benefits of selling a home.

Changes From the Tax Cuts and Jobs Act

The TCJA, enacted in December 2017, introduced several changes to mortgage interest and property tax deductions:

Mortgage Interest Deduction Limit:

- Before TCJA, homeowners could deduct mortgage interest on loan amounts up to $1 million.

- For mortgages taken out after December 15, 2017, the deduction is now capped at $750,000 ($375,000 for married couples filing separately).

- If you took out your mortgage before December 15, 2017, the $1 million limit still applies under the grandfather rule.

State and Local Tax (SALT) Deduction Cap:

- Before TCJA, homeowners could fully deduct state and local property taxes, along with income or sales taxes.

- Under TCJA, the total deduction for all state and local taxes (SALT), including property taxes, is now capped at $10,000 ($5,000 for married filing separately).

- This cap reduces the tax benefit of owning high-value properties in states with high property taxes.

Conclusion

While most closing costs aren’t directly tax-deductible, understanding which expenses qualify—such as mortgage interest, points, and property taxes—can help FSBO sellers maximize their tax savings. Keeping proper records and knowing how to itemize deductions ensures you don’t miss out on potential benefits.

If you’re selling your home FSBO and want a seamless, stress-free experience, PropBox can help. From managing offers to handling paperwork, PropBox simplifies the selling process so you can focus on maximizing your profits. Ready to take control of your home sale? Sign up for PropBox today and sell smarter!