When you choose to sell your home without an agent, you might feel overwhelmed by all the details involved, especially when it comes to handling the funds. This final step is where everything adds up, and it’s important to know what to expect. You’re in charge, and learning this process will help you feel more secure in your decision.

In this article, we break down the closing process into easy-to-follow steps that explain exactly how and when the money changes hands. With clear guidance, you’ll see that closing day doesn’t have to feel complicated. Keep reading to find out how to manage your home sale with clarity and confidence.

Why Understanding the Flow of Funds Matters

Understanding how money flows on closing day is essential because it’s when every payment is finalized—from the buyer’s deposit and loan funds to commissions, mortgage payoffs, and ultimately your proceeds. A closing agent or attorney oversees the distribution to make sure every dollar is properly accounted for.

When you're selling on your own, having a solid grasp on this process helps you track where each dollar goes and guarantees that you receive what you're owed. FSBO sales made up just 6% of all home sales in 2024, which makes it even more important to be informed so you can manage funds smoothly and prevent delays.

The Role of Escrow or Title Companies

Escrow and title companies serve as neutral third parties that hold funds and key documents during the closing process. Here’s an overview of how these professionals help ensure that every step, from fund deposits to document transfers, happens safely and according to plan:

Safeguarding Buyer and Seller Funds

Escrow accounts are designed to protect both you and the buyer by holding funds securely until all contractual conditions are met. Think of it as a safety deposit box where your money is kept safe until every requirement of the sale has been fulfilled. This system means that neither party gets paid until every agreed-upon detail like repairs, a clear title, or any other condition is satisfied. This minimizes the risk of fraud or accidental oversight.

Typical Payment Timeline

Understanding the sequence of payments on closing day is important for keeping your process efficient. Usually, the buyer makes an earnest money deposit within a few days of an accepted offer, which signals their commitment. Then, on closing day, these funds are disbursed to pay off any mortgages, cover fees, and deliver the remaining balance to you.

A strict timeline—typically spanning several weeks from offer acceptance to closing—ensures that funds are released only when every requirement is met, so you always know when to expect each payment. This predictable schedule not only provides financial clarity but also helps you coordinate final inspections and document signings smoothly.

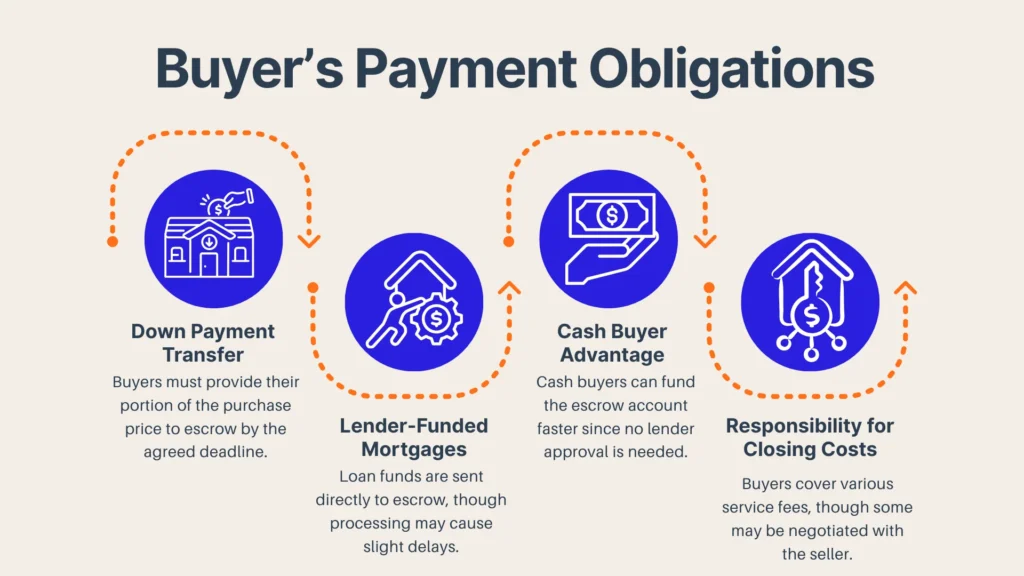

Buyer’s Payment Obligations

Buyers have their own set of responsibilities when it comes to providing payment. Their obligations include transferring the down payment and ensuring that any lender-provided funds are secured on time. Let’s break down what buyers typically need to do so you can anticipate when the money will be available for distribution:

Mortgage or Cash Payment

When a buyer is using financing, they’re typically relying on a lender to provide most of the purchase price for the home. Once the loan is approved, the lender sends those funds directly to the escrow company to complete the transaction. This extra step may sometimes introduce a slight delay as the lender verifies all the required details.

On the other hand, a cash buyer doesn’t need a lender, so they can transfer the full payment amount directly to the escrow account. This often speeds things up since there’s no need to wait on bank approvals or loan processing. So, while a cash buyer might have funds available in escrow sooner, buyers who need financing might experience slight delays as the lender finalizes everything on their end.

Closing Costs

Closing costs are fees that cover various services during the transaction, like loan origination, title insurance, appraisals, and administrative tasks. Since you’re handling the sale on your own, you save on agent commission fees, lowering your overall costs. Buyers and sellers may negotiate who covers which fees, which means you could end up sharing some of the costs.

Seller’s Net Proceeds

The seller’s net proceeds are the actual funds you take home after all expenses, fees, and debts have been deducted from the sale price. Here's a quick look at how these final numbers are calculated:

Paying Off Existing Mortgages or Liens

Before you receive any funds, any outstanding debts on your home must be settled, including mortgages, unpaid taxes, or contractor liens. The escrow company takes responsibility for ensuring that these amounts are paid off directly from the sale proceeds, so you don’t need to coordinate those payments yourself. This step is crucial for transferring a clear title to the new owner and for protecting your credit and reputation.

Calculating the Final Proceeds

Once all deductions have been made, what’s left is your final net proceeds. This calculation involves subtracting all closing costs, existing liens, and any negotiated fees from the total sale price. It’s essential to review your settlement statement carefully, ensuring every fee is accurate and giving you confidence that your final amount truly reflects your hard work—and your decision to avoid extra costs.

Payment Methods and Distribution

The distribution of funds at closing is managed securely by the escrow or title company, ensuring every dollar is accurately allocated. Let’s go over what you need to know about how these funds are distributed among creditors, the buyer’s lender, and you, as the seller:

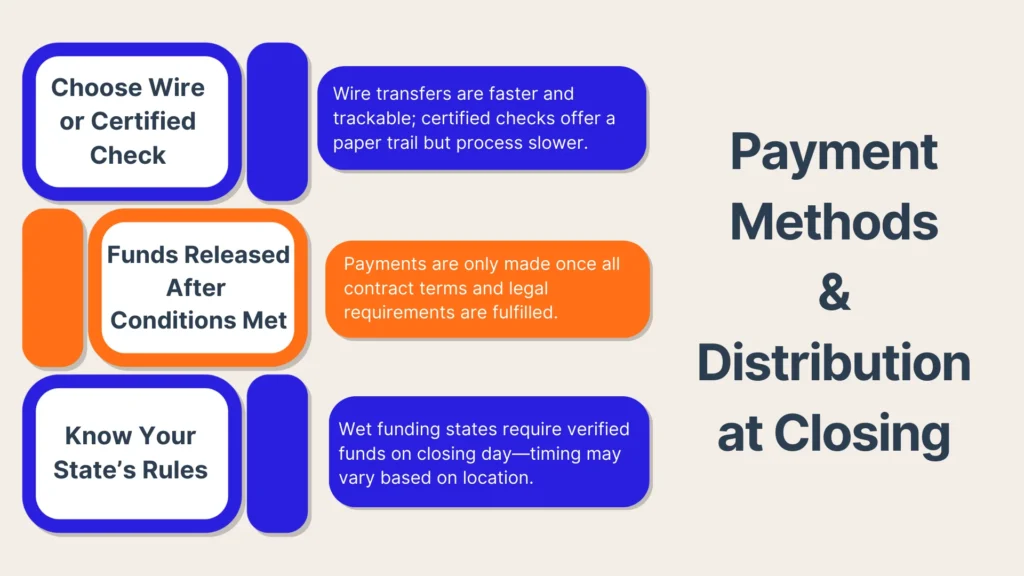

Wire Transfers vs. Certified Checks

When it comes to receiving your money, you might wonder whether a wire transfer or a certified check is best. Wire transfers are typically faster and offer a secure, electronic record of the transaction, and they let you track your funds almost instantly, which is especially useful when dealing with large amounts.

Certified checks, on the other hand, provide a robust paper trail and a sense of physical verification; however, they usually take a bit longer to process. Because of the delay, certified checks can be less convenient—especially when time matters—so many sellers opt for wire transfers instead.

Timing of Fund Release

Funds are released only after all the conditions in the contract have been fully met, and local or state laws can affect exactly when that happens. For example, in wet funding states like New Jersey and Pennsylvania, banks require all funds to be verified and available on the actual day of closing. This means any checks must clear and physical funds must be confirmed before anything is officially paid out.

This process helps prevent premature payments and gives both parties time to meet their responsibilities without rushing. It also gives escrow companies a clear framework for handling final disbursements. If there’s a delay—like missing paperwork or an issue with the buyer’s loan—the funds will stay in escrow until everything is resolved. Knowing how your state handles funding helps you know what to expect and avoid last-minute surprises at closing.

Adjustments and Prorations

Adjustments are one-time corrections, such as reimbursing a buyer for prepaid expenses, while prorations evenly divide recurring costs like property taxes, HOA dues, and utilities according to the period each party owns the property. This approach ensures that both you and the buyer pay only for the time you actually own the home.

It’s important to understand that these calculations will be clearly outlined in your settlement statement, so you get a full picture of any financial responsibilities before closing. Here are the details to keep in mind as you continue through the settlement process:

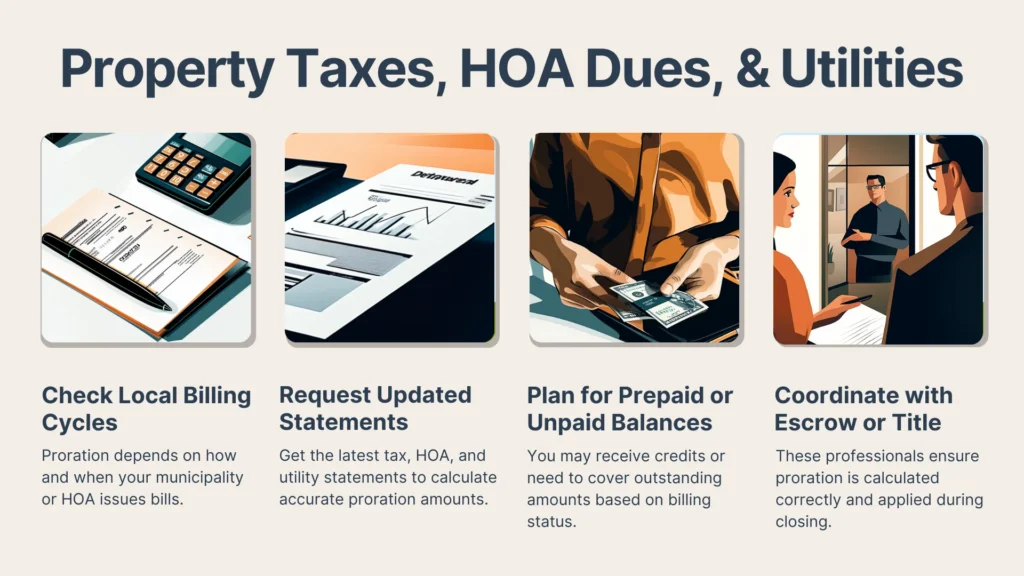

Property Taxes, HOA Dues, and Utilities

Recurring expenses such as property taxes, HOA dues, and utility bills are usually split between the buyer and the seller through proration, meaning each party pays only for the period they own the home rather than the full billing cycle.

For example, if annual property taxes have been paid in full but the home sells mid-year, the seller typically gets a credit for the unused months while the buyer assumes responsibility for the remaining balance. In fact, a recent report noted that about 10% of FSBO sellers found managing these prorated expenses challenging, which is why understanding proration can help you avoid confusion and surprise charges at closing.

Final Settlement Statement Review

Before signing the final documents, you must review the settlement statement with a fine-tooth comb. This statement summarizes every credit and debit involved in the transaction, so double-check that there are no hidden fees or miscalculations. By taking this extra step, you protect your interests and ensure you receive every dollar you’re due.

Conclusion

Selling your home on your own might seem challenging, but understanding how funds are paid at closing makes the process much more manageable. By familiarizing yourself with escrow procedures, keeping a strict payment timeline, and knowing how to handle closing costs and adjustments, you’ll gain the confidence to control every step of your sale.

With Propbox, you can simplify your entire FSBO process further, from organizing paperwork to automating reminders, saving you time and reducing stress while keeping more of your hard-earned money. Try Propbox today to maximize your profits and stay organized!