Buying or selling a home can feel overwhelming, especially if you're new to it. With so many steps and unfamiliar terms, the process can seem complicated. One of those terms is the mortgage escrow process. It sounds confusing, but it's simpler than you think.

Escrow is a key part of real estate transactions that helps protect both buyers and sellers. Knowing how it works can give you more confidence and make the process a lot easier. If you're new to selling a home, understanding escrow can help you feel more prepared and in control throughout the process.

In this article, we'll explain what mortgage escrow is, why it matters, and how it can help you manage your home sale with confidence.

What Is Mortgage Escrow?

Mortgage escrow refers to an arrangement where a neutral third party holds funds, documents, and key paperwork during a real estate transaction. This ensures all conditions agreed upon in a home sale are properly met before money or property ownership is officially transferred.

The primary purpose of escrow is to protect both buyers and sellers. For example, if a buyer must make repairs before closing, escrow can hold the funds until the work is finished. This ensures everyone gets what they agreed to, keeping the process fair and secure.

The Basics of Escrow in Real Estate

Escrow is a crucial step in virtually every home sale, providing assurance and security for everyone involved. To understand escrow clearly, let's dive into the essential details of how it functions and why it’s necessary.

Escrow as a Third-Party Holding System

The escrow account securely holds earnest money, documents, and contracts during the transaction. This protects both parties if unexpected issues arise, like financing problems or inspection concerns, offering legal and financial safeguards to reduce disputes.

Common Escrow Terminology

Understanding some common escrow terms can make the process easier to follow and give you more confidence in handling your home sale. When dealing with escrow, you'll likely encounter these terms:

- Escrow Officer/Agent: The impartial third party managing your escrow account.

- Earnest Money: A deposit provided by buyers to show they’re committed to buying the property.

- Contingencies: Specific conditions that must be fulfilled before completing the sale, like inspections, appraisals, or securing financing.

- Title Search: A review of property records to confirm legal ownership and identify any potential liens or claims against the property.

- Closing Costs: Expenses beyond the home's price that buyers and sellers pay at closing, including lender fees, title insurance, and taxes.

Setting Up an Escrow Account

Once your escrow account is set up, it becomes the go-to place for managing all the important parts of your home sale. It keeps everything on track, making sure deadlines are met and paperwork is in order. Setting up escrow the right way can help avoid unnecessary delays and last-minute surprises.

Choosing an Escrow Service

You can establish escrow through title companies, banks, or escrow-specific agencies. Consider factors like cost, reputation, and familiarity with local regulations when selecting a service. Since you're selling your home without an agent, choosing an escrow provider experienced in FSBO transactions can help keep the process smooth and organized.

Initial Funding (Earnest Money Deposit)

Once an offer is accepted on your home, the buyer will put down an earnest money deposit in the escrow account. It’s their way of showing they’re serious about the purchase and ready to move forward, giving you peace of mind that things are on track.

Required Documentation

As someone selling their home without an agent (FSBO), you're in the 6% of homeowners taking on this process themselves, which means preparation is key. Double-checking every document is crucial to keeping things moving smoothly.

Keep detailed records of key documents such as the purchase agreement, property disclosures, and financing details. Organize repair receipts, inspection reports, and warranties for appliances or systems like plumbing, HVAC, and roofing. Providing these upfront helps answer buyer questions and builds trust in the closing process.

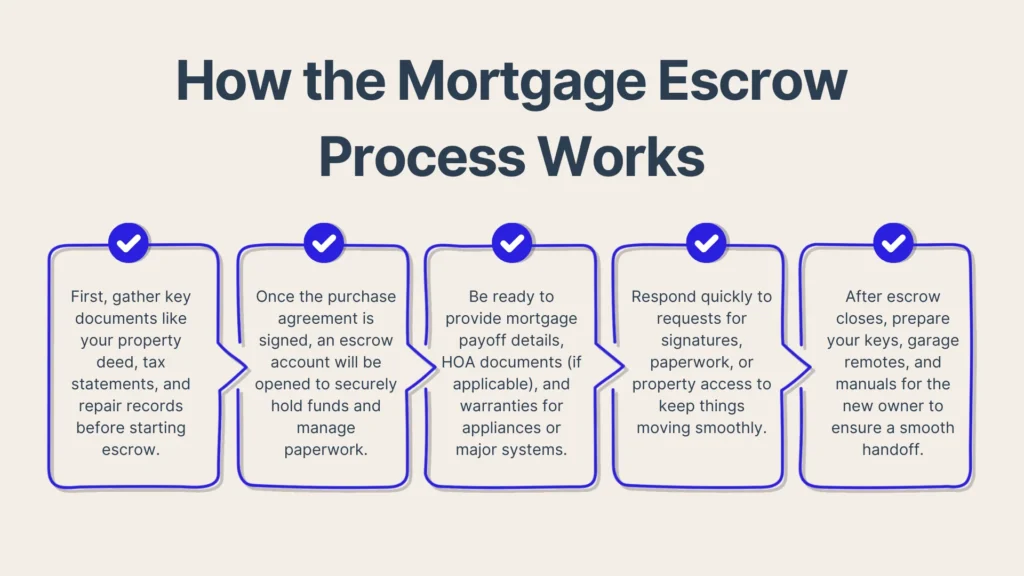

How the Mortgage Escrow Process Works

The escrow process is really just a step-by-step system designed to protect both you and the buyer. We'll walk through each step so you know what to expect and can stay prepared for anything that comes up.

Step-by-Step Timeline

Every step of escrow keeps your home sale moving forward. From accepting an offer to finalizing all the paperwork, understanding the process can make things feel more manageable.

- Signing the Purchase Agreement: The buyer and seller agree on terms like price, contingencies, and deadlines. Since this contract guides the entire process, reviewing it carefully helps avoid delays.

- Depositing Earnest Money: The buyer submits a deposit (usually 1-3% of the home price) into escrow. This shows they’re serious about buying and protects you if they back out without a valid reason.

- Inspection, Appraisal, and Title Search: These steps confirm the home’s condition, value, and legal ownership. If issues arise, they may need to be resolved before closing.

- Satisfying Contingencies: The buyer must meet conditions like securing financing or requesting repairs. Quick responses from you can help keep things moving.

- Finalizing the Mortgage and Closing: The final paperwork is completed, the buyer’s loan is approved, and funds are transferred. Once everything is verified, escrow closes, and you receive your payment.

Role of the Escrow Agent or Officer

Escrow agents work behind the scenes to keep things on track. They primarily coordinate with lenders, title companies, and legal advisors to make sure everything follows the rules. They also help clear up miscommunications, handle issues that pop up, and guide the process from start to finish.

Seller’s Perspective During Escrow

Staying organized and responding quickly to buyer requests helps keep escrow on track. Delays can happen if paperwork is missing or contingencies are unresolved, especially as the closing process typically moves quickly. Having your documents ready and addressing issues promptly speeds things up and prevents last-minute hiccups.

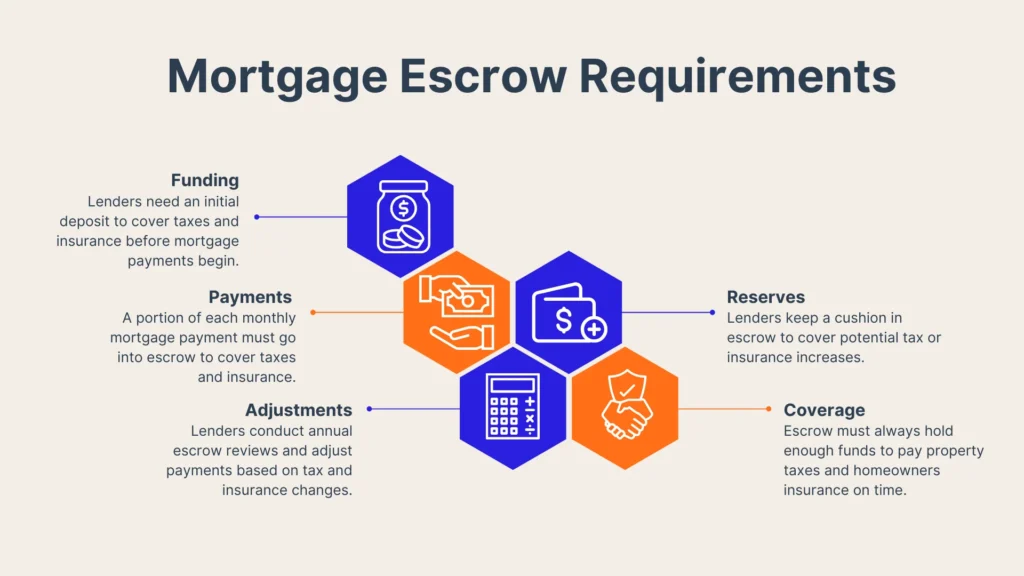

Mortgage Escrow Requirements

Escrow isn’t just about holding funds; it also plays an ongoing role in homeownership. Many lenders require escrow accounts to ensure property taxes and insurance are paid on time, helping you avoid late fees or lapses in coverage. Here’s what you need to know about lender-imposed escrow accounts.

Lender-Imposed Escrow

Lenders often require escrow accounts to cover property taxes, homeowners insurance, and mortgage insurance. Each month, a portion of your mortgage payment goes into this account. When those bills are due, the lender uses these funds to pay them, ensuring everything stays current to protect both their investment and your home.

Calculating Monthly Escrow Payments

Escrow payments are based on estimated yearly costs for property taxes, homeowners insurance, and mortgage insurance, divided into monthly payments. Since these costs can change, your escrow contribution may adjust each year to reflect the updated amounts, helping you stay on top of your expenses.

For example, if your property taxes increase by $600 for the year, your lender may raise your monthly escrow payment by $50 to cover the difference. This adjustment helps ensure there’s enough in your escrow account to pay future bills.

Escrow Cushion or Reserve

Lenders keep a cushion of extra funds in your escrow account to prevent shortages if property taxes or insurance premiums increase. This reserve helps cover unexpected costs, so you’re not left paying the difference out of pocket. It’s designed to keep your escrow account stable and ensure your bills are covered.

Common Contingencies and Their Impact on Escrow

Contingencies are safeguards built into the home sale process, helping protect both buyers and sellers from unexpected issues. Since about 17% of FSBO sellers struggle with pricing and 13% face challenges selling within their desired timeframe, contingencies can impact how smoothly a transaction moves through escrow.

Inspection and Repair Negotiations

If the inspection reveals issues, buyers may request repairs or a price reduction. Resolving these quickly helps keep the escrow on track. Offering repair credits instead of fixing issues yourself can also speed up the process and give buyers more flexibility.

Appraisal Contingency

An appraisal verifies the home's value for the lender. If it comes in low, buyers and sellers can renegotiate by lowering the price, offering seller concessions, or having the buyer make up the difference in cash. Another option is requesting a second appraisal or challenging the initial one with stronger comparables.

Financing Contingency

Buyers must secure financing within a set timeframe to keep escrow on track. If delays occur, sellers can grant an extension or request proof of lender progress. If financing falls through, the deal may be canceled, and the buyer risks losing their earnest money deposit.

Closing the Escrow

The final stage of escrow ensures everything is in place before ownership officially transfers. With most homes closing in about three weeks, confirming all conditions are met and addressing any last-minute details helps prevent delays. Here’s what to expect in the final steps of escrow.

Final Walk-Through

Before closing, buyers inspect the property one final time, verifying that repairs were completed and conditions remain as agreed upon. If issues arise, this walkthrough gives sellers a chance to address concerns before they delay the closing process.

The Closing Disclosure (CD)

Review the Closing Disclosure carefully prior to signing, as it outlines the final loan terms, settlement charges, and any outstanding balances. Be sure to double-check your payoff amount, confirm any agreed-upon credits, and verify that all charges are accurate to avoid unexpected costs or delays.

Signing and Funding

On closing day, you'll sign all the required documents, and funds will be transferred simultaneously. The escrow agent will then distribute the money, paying you, the lender, and any other involved parties. Once the funds and title are exchanged, escrow will officially close.

Conclusion

Understanding the mortgage escrow process empowers you to navigate selling your home with confidence and clarity. While about 88% of homebuyers rely on real estate agents, exploring alternatives like FSBO can help avoid typical agent fees of around 6%. Platforms like PropBox make this FSBO process easier, faster, and simpler.

PropBox takes the stress out of selling by automating reminders, organizing documents, and streamlining listings. With a smoother process and fewer headaches, you can sell quickly, protect your interests, and get the best value for your home.