Selling your home on your own without a real estate agent can save you money, but figuring out the closing process can feel overwhelming, especially if you're new to it. If you're a first-time seller tackling a "For Sale By Owner" deal, you might be unsure how to handle negotiations, paperwork, or legal details without guidance.

Don't worry: understanding the closing process isn't as complicated as it might seem. In this article, we'll walk you through each step clearly and simply, so you can move confidently from accepting an offer to handing over the keys.

A Brief Overview of the Closing Process

Closing, sometimes called settlement, is the final phase of a real estate sale. It involves signing documents, transferring funds, and confirming that the title is ready to be passed from seller to buyer. Every detail that has been negotiated, such as price adjustments, repairs, or specific contract terms, becomes official at this stage.

Here's a table that outlines the typical timeline of the real estate closing process for FSBO sellers, along with relevant statistics at each stage:

| Stage | Timeline | Key Actions | Statistics |

| Preparation | Day 1-7 | Decide to sell, choose FSBO, and prepare a house. | 5% of FSBO listings get the asking price. |

| Opening Escrow | Day 8 | Open escrow, and deposit earnest money. | 90% of transactions use an escrow service. |

| Due Diligence | Day 9-20 | Inspections, appraisals, contingencies. | 25% of deals face delays due to failed inspections. |

| Document Gathering | Day 21-25 | Gather necessary legal and financial documents. | FSBO sellers spend 20+ hours on paperwork. |

| Final Walk-Through | Day 26 | Final inspection by a buyer to verify condition. | 10% of sales falter at the final walk-through. |

| Signing Day | Day 27 | Sign all closing documents, and verify funds. | 98% of sales proceed after signing day. |

| Closing and Recording | Day 28 | Documents are filed with county, ownership transfers. | Sales are recorded within 24 hours of finalization. |

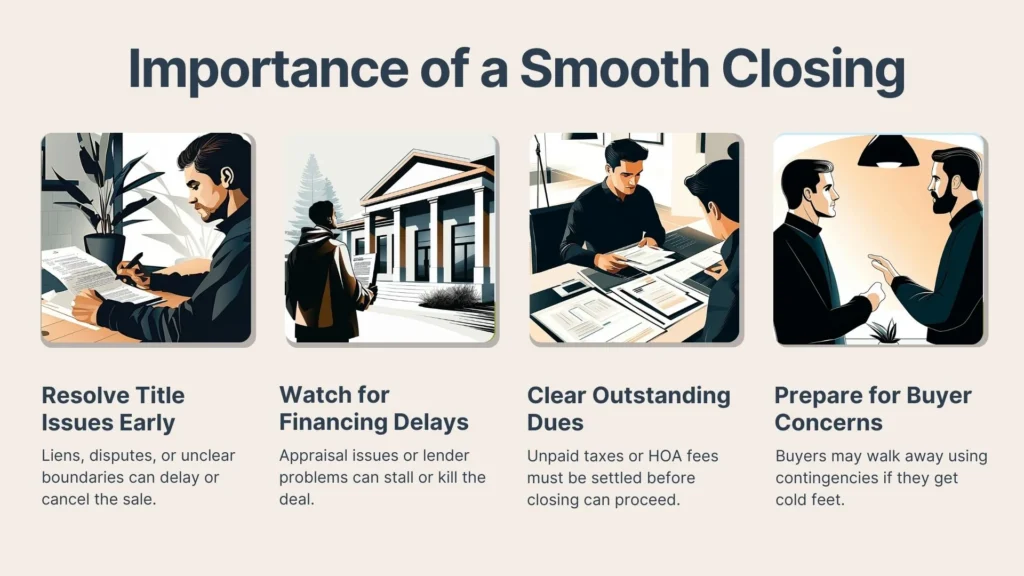

Importance of a Smooth Closing

Several factors can disrupt a closing if not addressed early. Common deal breakers include title issues, financing delays, unpaid property taxes, and last-minute buyer concerns.

- A clean title is necessary for closing, but issues such as unresolved liens, ownership disputes, or unclear property boundaries can delay or cancel the sale.

- Financing delays often arise when buyers rely on mortgage approval. A low appraisal can force price renegotiations, while debt-to-income changes or missing paperwork may cause the lender to reject the loan.

- Unpaid property taxes or HOA fees can also cause closing delays. Buyers expect sellers to settle these costs, and any outstanding balances must be cleared before ownership transfers.

- Finally, buyer cold feet can derail a deal, even when everything appears on track. If buyers reconsider for financial or personal reasons, they may use contingencies to walk away without penalty.

Key Players in the Closing

Several people play a role in closing a home sale. For you, the seller, understanding these roles is especially important since there is no agent coordinating the final steps.

Title Company or Escrow Agent

The title company or escrow agent acts as a neutral third party that holds funds and ensures that all contract conditions are met. When someone refers to “escrow,” they are talking about this entity.

Title companies also verify ownership, check for outstanding liens, and prepare the necessary paperwork to legally transfer ownership.

Attorneys (If Required by State)

Some states require that an attorney oversee real estate transactions. Even in states where it is not mandatory, some FSBO sellers choose to hire an attorney for legal guidance.

Having legal support is especially useful for unique circumstances, such as selling an inherited property or handling a sale during a divorce. Some attorneys charge a flat fee for reviewing documents, while others charge by the hour.

Lender (If Applicable)

When a buyer takes out a mortgage, the lender plays a significant role in closing. Lenders require appraisals to confirm the home’s value and often request additional paperwork from both the buyer and seller.

Keeping an open line of communication with the lender helps keep the transaction on schedule. You may need to provide certain documents or allow access to inspections and appraisals.

Preparing for Closing

Being prepared can make the difference between a fast closing and one filled with delays. Let’s take a look at different things you can do ahead to stay prepared:

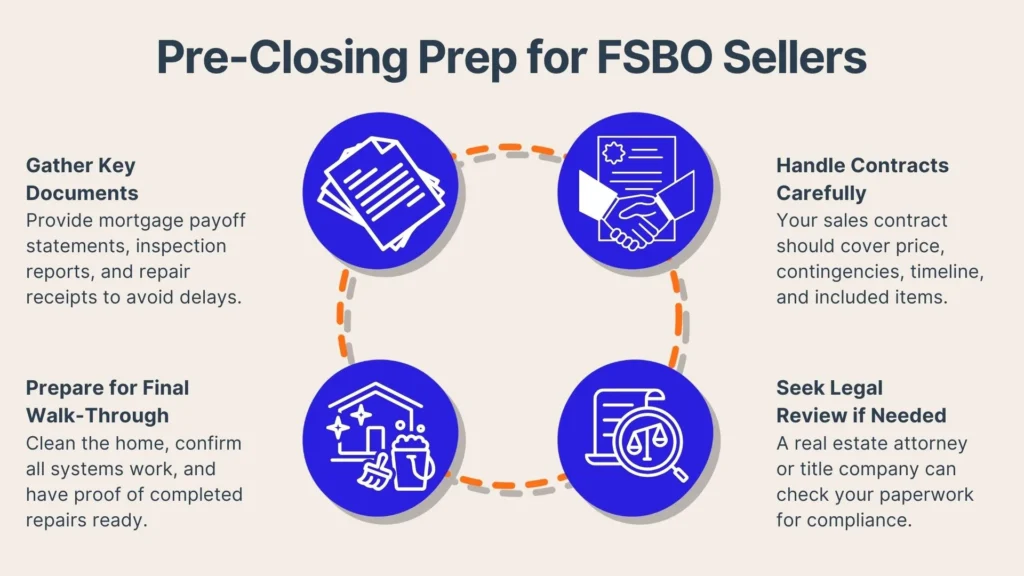

Assembling Required Documents

Before closing, buyers and title companies will request several documents to finalize the sale. Payoff statements are necessary if the home still has a mortgage, as they confirm the exact amount needed to close out the loan. Buyers may also ask for inspection reports to review any past findings and confirm that all disclosed issues have been properly addressed.

If repairs were part of the negotiation, keeping receipts and invoices as proof ensures transparency and avoids last-minute disputes.

Scheduling a Final Walk-Through

Buyers typically request a final walk-through 24 to 48 hours before closing to confirm the home's condition and completed repairs. Prepare by cleaning, ensuring major systems and appliances work, providing repair receipts, and removing personal items not included in the sale.

FSBO Seller Preparations

Selling a home without an agent means handling key documents yourself. The sales contract should clearly outline the purchase price, contingencies, closing timeline, and any included property items. To avoid legal issues, you can have a real estate attorney or title company review the contract for accuracy and compliance with local laws.

Understanding Closing Costs and Fees

Closing costs can vary depending on the state and local regulations, but they typically amount to two to five percent of the home’s sale price. Sellers should be aware of common costs and how they are split between buyer and seller:

Common Seller Fees

Sellers are usually responsible for:

- Title Search and Insurance: This ensures the buyer receives a clear title.

- Transfer Taxes: Some states and cities charge a tax when property ownership is transferred.

- Attorney Fees: If legal representation is required, the seller covers this cost.

- Outstanding Liens or Mortgages: Any remaining balances on the property must be paid off before closing.

The Role of Escrow

Escrow acts as a neutral third party that manages funds and documents until all conditions of the sale are met.

- Holds funds safely: Manages deposits, purchase funds, and loan payoffs.

- Oversees document handling: Ensures all required paperwork is signed and recorded.

- Clears financial obligations: Pays off existing mortgages, liens, and other closing costs.

- Finalizes the transaction: Releases funds and transfers ownership once all terms are met.

Tips for Budgeting

Reviewing key documents and setting aside extra funds will keep the process smooth and avoid last-minute surprises.

- Set aside extra funds: Prepare for unexpected expenses to avoid last-minute stress.

- Review the closing disclosure early: Check final costs in advance to prevent surprises.

- Save for closing costs: Plan for taxes, fees, and other expenses.

- Double-check moving costs: Factor in transportation, storage, and utility setup.

- Keep extra money for home repairs: Address any last-minute fixes or maintenance needs.

Step-by-Step Closing Process

Closing is the final stage of selling a home, and understanding each step can help you feel prepared. While the process might feel paperwork-heavy, approaching it in an organized way can keep things moving smoothly.

Reviewing the Closing Disclosure (CD)

The closing disclosure (CD) outlines the final sale details, including fees, taxes, and agreed-upon credits. Buyers receive it at least three days before closing, while sellers typically get a settlement statement with similar information.

Review the sale price, taxes, and credits to confirm they match expectations. Check for errors like incorrect loan payoffs or duplicate fees, and address any discrepancies before closing day.

Signing Final Paperwork

On closing day, both parties sign documents to finalize the sale. Key documents for sellers include:

- Deed Transfer: Transfers home ownership to the buyer.

- Bill of Sale: Lists any included personal property.

- Payoff Authorization: Allows the escrow agent to pay off any remaining mortgage.

Sellers must provide ID, and all listed owners must sign unless prior arrangements are made. Once complete, the transaction moves to the final financial stage.

Once all the paperwork is complete, the transaction moves to the final financial stage.

Disbursing Funds

Once everything is signed, the escrow agent or attorney will handle the distribution of funds.

- Mortgage Payoff: If there is still a loan on the property, the lender receives the necessary amount to close the loan.

- Outstanding Liens or Taxes: If there are unpaid property taxes, utility bills, or liens, those are deducted from the proceeds.

- Closing Costs: Any fees owed to the title company, attorney, or other service providers are paid at this time.

- Seller’s Net Proceeds: The remaining amount goes to the seller, either as a wire transfer or a cashier’s check.

This step is usually completed on the same day as closing, but in some cases, it may take a day or two for funds to clear. You should confirm with their bank when to expect the proceeds to be available.

Recording the Deed

The final step in the closing process is recording the deed. The escrow agent or title company submits the signed deed to the local county recorder’s office, making the transfer of ownership official. This public record confirms that the buyer is now the legal owner of the property.

Once the deed is recorded, the seller no longer has legal responsibility for the home. If the seller needs proof of the completed sale for tax or financial purposes, a copy of the recorded deed can usually be requested from the county office. With this step completed, the home sale is officially done.

Post-Closing Responsibilities

Although closing day marks the official transfer of the home, sellers still have a few tasks to wrap up after the sale. Taking care of these responsibilities quickly will help avoid unnecessary complications and allow a smoother transition for both parties:

Moving Out and Turning Over Keys

You should plan their move-out timeline to align with the closing date unless other arrangements have been made with the buyer. In most cases, sellers must vacate the property before closing, though some contracts allow a short post-closing occupancy period.

When turning over the property, sellers should provide all keys, garage door openers, and access codes. If the home has smart locks or security systems, it is courteous to reset them and provide clear instructions for the buyer. Some sellers also leave a small packet with appliance manuals, warranty information, or helpful neighborhood details.

Retaining Records

Keeping key closing documents is important for taxes, legal matters, and future property purchases. Essential records include the settlement statement or closing disclosure for financial details, the deed transfer copy as proof of ownership, mortgage payoff confirmation, and receipts for repairs or improvements for tax or warranty purposes.

Store both physical and digital copies for security. Tax professionals suggest keeping records for at least seven years, while the deed should be kept permanently.

Addressing Disputes (If Any)

While most sales go smoothly, buyers may raise concerns after closing. Common disputes include undisclosed property damage, where buyers may seek repairs or legal action, disagreements over included items like appliances or fixtures, and boundary or easement issues discovered through surveys.

Conclusion

Understanding each phase of the real estate closing process can simplify the complexities involved in selling your property. This guide, equipped with real-life examples, simple checklists, and detailed tables, offers practical and easy-to-follow guidance to ensure a smooth transition of ownership with minimized stress and maximized success.

Want an even smoother experience? Streamline your property sale with PropBox, the essential tool for FSBO sellers looking to enhance efficiency and accuracy. PropBox simplifies document handling and improves communication, leading to a smoother, quicker closing process and a better overall selling experience.