Selling your home is exciting, but unexpected problems at closing can quickly turn excitement into stress. One of the most common issues sellers face involves the property title, and even small problems can delay or cancel your sale altogether.

This article covers everything you need to know about title issues, from spotting common red flags to fixing them before they impact your closing. We'll walk you through the process step by step, so you know exactly what to watch out for and how to resolve any surprises.

Why Title Issues Matter

The “title” to a property is the legal record of who owns it and who might have a claim to it. A clean title means no other parties can step forward, saying they have a stake in the home. Without that clean record, buyers can’t confidently proceed, lenders won’t approve financing, and your deal may come to a sudden halt.

Title issues can delay, complicate, or even cancel a home sale. That means if something is off, you’re the one responsible for fixing it. According to the National Association of Realtors, about 13% of FSBO sellers cite “selling within the planned timeframe” as a top challenge, and title problems can be a big part of that.

Common Title Issues That Can Arise

Even if your home has been in your name for years, problems may be hiding in the background. Some of these don’t surface until a title search is done, often late in the process, when buyers are already lined up and timelines are tight. These are some of the most common problems that can crop up:

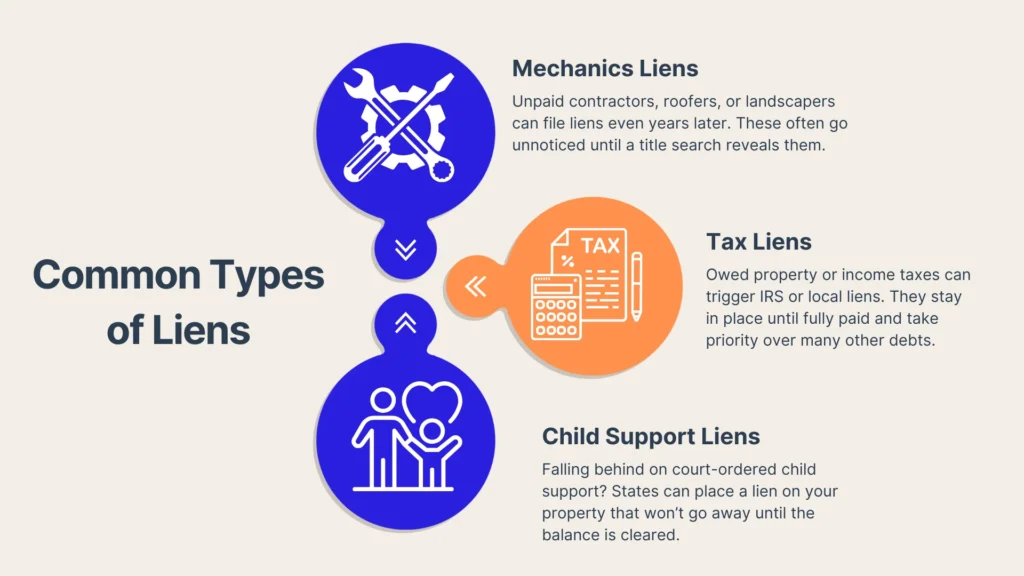

Outstanding Liens or Judgments

Liens are legal claims against your property, usually tied to unpaid debts. They don’t disappear when the property changes hands, which is why they must be addressed before closing. Even if the debt isn’t yours, a lien from a previous owner or an old contractor can still hold up your sale. Here’s a closer look at the most common types:

- Mechanics liens: These come from contractors, subcontractors, or suppliers who worked on your home and didn’t receive full payment. Even if the work happened years ago, the lien might still be attached to the title if it was never cleared. This can include unpaid roofing jobs, kitchen remodels, plumbing work, or landscaping. Sometimes, homeowners aren't even aware the lien exists until it shows up during the title search.

- Tax liens: These are placed by the IRS or local government when property taxes or income taxes are past due. A tax lien takes priority over many other debts, which can make it especially serious in a real estate transaction. Even if you’ve entered into a payment plan with the tax authority, the lien will remain in place until the debt is fully paid and released.

- Child support liens: If a person responsible for child support has fallen behind on payments, the state can place a lien on any property they own. These liens are often filed through family court systems and stay attached to the title until cleared. In some cases, the property owner may not even know the lien was recorded, especially if the paperwork was missed or delivered incorrectly.

Even if you’re unaware they exist, they follow the property and not just the person. Clearing them usually involves paying off the debt or negotiating a reduced payoff. Depending on the lien type and the responsiveness of the creditor, it can take anywhere from a few days to several weeks.

Boundary Disputes and Survey Errors

If your neighbor believes your fence crosses into their yard or if your property line hasn’t been properly marked since the 1980s, that’s a red flag. Boundary issues can come up during a new survey ordered by the buyer’s lender, leading to confusion or disagreement. Updated surveys are your best tool for avoiding surprises and clearing up misrepresentations about lot size or use.

Missing or Incorrect Ownership Records

Sometimes, a long-lost co-owner, an heir, or even a typo in a deed can cause ownership concerns. For instance, if a previous owner passed away and the estate wasn’t settled correctly, the title might still reflect partial ownership by someone else. Similarly, something as small as a misspelled name or incorrect marital status in county records can throw the whole deal off course.

Conducting a Thorough Title Search

Catching these issues early gives you the time and space to resolve them before a buyer is involved, and typically, a title search is your first line of defense. Keep these points in mind during a title search:

Reviewing Public Records

During the title search, the following documents are reviewed:

- Deeds to trace ownership

- Mortgages to verify they’ve been released

- Easements that allow others to access part of the land

- Encumbrances like liens or restrictive covenants

Each of these documents tells part of your home’s story, and catching an issue in them ASAP can save you from panicked phone calls later.

FSBO Seller’s Responsibility

If you're selling your home on your own, it’s easy to assume the buyer or their agent is handling the title work. However, about 10% of sellers in your position say paperwork is one of the most confusing parts of the process, and title issues often play a role. Taking the time to check that your title is clear before listing can help prevent delays later.

Role of a Title Company or Attorney

Most sellers work with a title company or real estate attorney to search public records. These professionals comb through deeds, tax records, court judgments, and more to spot any problems. The typical cost of a title search runs between $200 and $400, depending on your location and how complex the records are.

Title Insurance – Why It’s Essential

Once the title is verified, there’s one more important piece of protection: title insurance. This isn't just paperwork, it’s a safeguard for what you and your buyer are investing in:

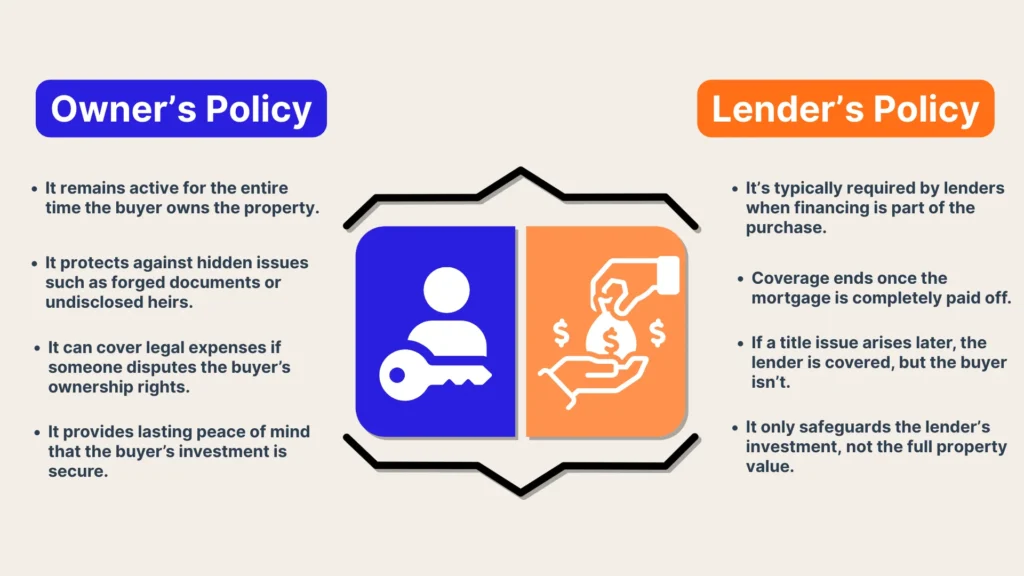

Owner’s Policy vs. Lender’s Policy

There are two main types of title insurance in a real estate sale. Each one serves a different purpose, and knowing the difference can help you avoid confusion at closing.

Owner's Policy

This insurance protects the buyer's ownership interest in the property. It provides coverage for the full purchase price, not just the loan amount.

- It stays in effect for as long as the buyer owns the home.

- It covers hidden problems like forged signatures, errors in public records, or unknown heirs.

- It helps pay legal costs if someone challenges the buyer’s right to the property.

- It gives long-term peace of mind that your investment is protected

Without an owner's policy, you could end up paying out of pocket if a hidden title problem shows up after closing. Buyers often feel more comfortable when they know you’ve taken steps to protect the deal with title insurance.

Lender's Policy

This type of insurance protects the mortgage lender. It does not protect the buyer, even though the buyer usually pays for it as part of closing costs. Note the following points:

- Most lenders require it when a mortgage is involved.

- It only covers the amount the lender loaned for the purchase.

- If a title problem shows up later, the lender is protected, but the buyer is not.

- This policy ends once the loan is fully paid off.

Protection Against Hidden Risks

Even with a detailed title search, some problems can remain hidden until after closing.

- Unknown heirs of previous owners: A former owner may have passed away without all heirs being notified. If someone later claims a right to the property, it can lead to legal trouble for the new owner.

- Forged signatures in the chain of title: Someone may have faked a signature on a past deed or legal document. This can create questions about whether the property was legally transferred.

- Undisclosed easements or rights of access: A company or neighbor may have legal access to part of the land that was never recorded properly. This could affect how the buyer uses the property after the sale.

Title insurance provides peace of mind in the face of these hidden risks. It acts as a safety net if something emerges later that wasn’t in the public record at the time of sale.

Cost and Negotiation Considerations

Expect title insurance to cost somewhere between $500 and $1,500. Whether you pay for it, split it, or pass it to the buyer often depends on local customs, so it’s helpful to know what’s typical where you’re selling. Taking a few minutes to research what’s standard in your area can make negotiations smoother and help avoid any back-and-forth at closing.

Resolving Title Issues Before Closing

Discovering a title issue doesn’t have to mean disaster. Many problems can be resolved with the right steps and a bit of lead time. Resolve these matters quickly for a fuss-free closing:

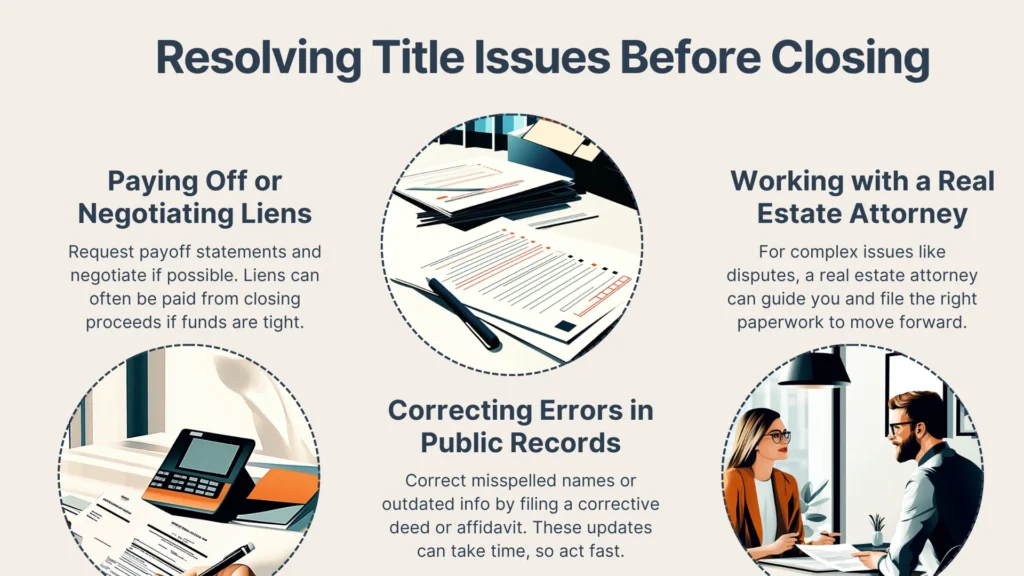

Paying Off or Negotiating Liens

Start by requesting payoff statements for any outstanding liens. In some cases, you can negotiate a lower amount, especially if the lien is old or disputed. If funds are tight, you might arrange to have the lien paid at closing from your proceeds.

Correcting Errors in Public Records

If a deed needs a name correction or a past error needs updating, you may need to file a “corrective deed” or an affidavit with your county recorder’s office. Depending on the backlog, these updates can take days or weeks to appear in official records. That’s why catching them early really helps.

Working with a Real Estate Attorney

Some issues are best handled with legal support. This is especially true for contested claims, inheritance disputes, or long-standing boundary conflicts. A real estate attorney can help draft legal solutions, negotiate with other parties, and provide the necessary filings to move your sale forward.

Consequences of Unresolved Title Problems

When title issues aren’t addressed in time, the impact can ripple far beyond a delayed sale:

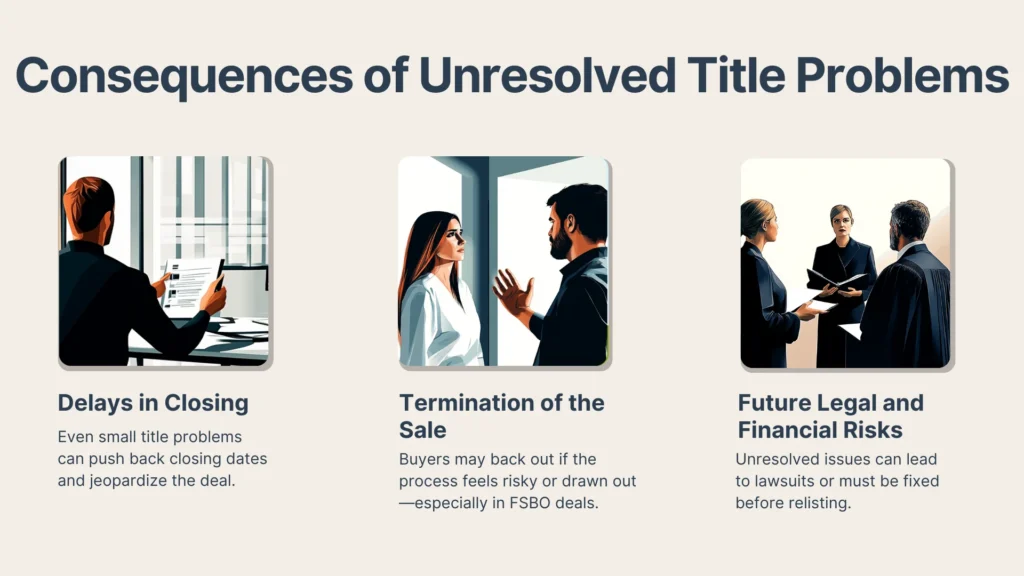

Delays in Closing

Even minor title issues can lead to extended closing timelines. If your buyer has locked in an interest rate or scheduled a move, delays can quickly become deal-breakers. These situations create stress and frustration for everyone involved.

Termination of the Sale

Buyers may walk away if they feel the transaction is dragging or complicated. In FSBO situations, this is even more likely since the buyer may feel less protected. Worse yet, word can spread, impacting your reputation if you're selling in a small or tight-knit market.

Future Legal and Financial Risks

Leaving a title issue unresolved doesn’t make it go away. If you do manage to sell the home without disclosing a known issue, you could face legal action down the line. And if the sale falls through, you’ll still need to fix the problem before relisting.

Conclusion

From checking public records to spotting red flags early and knowing how title insurance works, you're not just protecting the deal, you’re setting yourself up for a smoother, more confident sale. Propbox makes it easy by giving you an organized, step-by-step process with built-in tools to help you stay ahead of common problems like title issues.

If you’re ready to sell without the 6% fee but want to feel supported every step of the way, start with Propbox. Your sale and your control are backed by smart tools that help you close without stress.