Selling your home alone means tackling legal and financial details that real estate agents usually handle. Amongst those details, a property lien is one of the most important things to note, yet it often gets overlooked.

What is a property lien, and how can it impact your FSBO sale? In this guide, we’ll break down everything FSBO sellers need to know about property liens, such as what they are, how to handle them, and how to keep your sale on track.

Understanding Property Liens

A property lien is a legal claim against a home or piece of real estate, typically used as collateral to ensure a debt gets paid. Liens can seriously delay—or even derail—a sale if not addressed early.

A title search is usually done by the buyer’s attorney or title company, and this process will uncover existing liens. If one appears, you must resolve it before the sale progresses. That might mean paying off the debt, negotiating a settlement, or disputing the lien if incorrect. Either way, finding out about liens before listing your home is best.

How Do Liens Work?

When a lien is placed on a property, the owner cannot transfer ownership until the lien is cleared. Simply put, it’s like a red flag on your title that says, “There’s a debt here that needs attention.”

The lien gives the creditor legal rights to your property, though they can’t just take it immediately. Instead, the lien serves as security. If you try to sell the home, the lien must be paid from the sale proceeds before the buyer can take ownership. Resolving liens beforehand means a smoother, faster closing process for FSBO sellers.

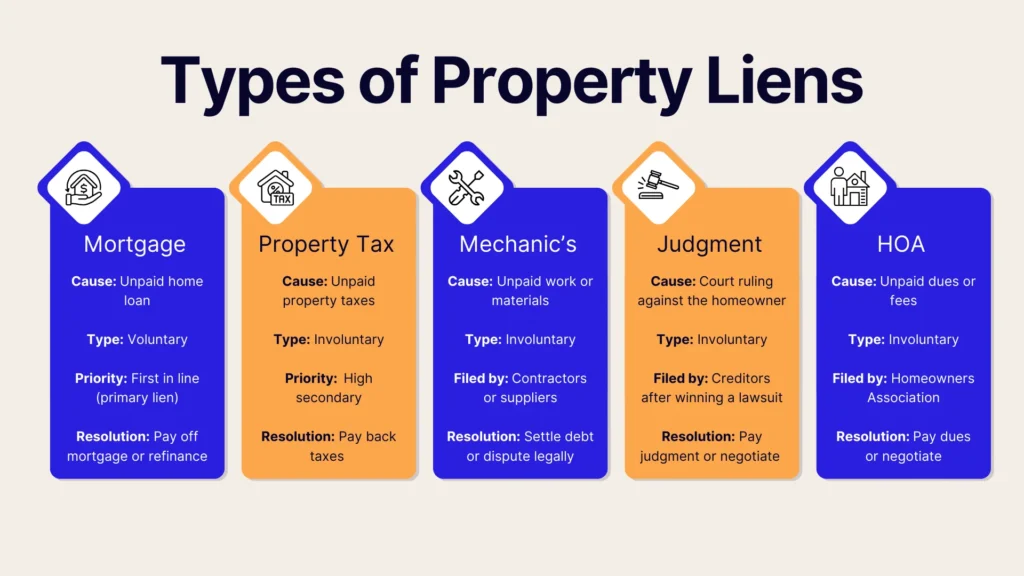

Types of Property Liens FSBO Sellers Should Know

Before selling your home FSBO, it’s essential to understand the different types of property liens that could affect your transaction. Some liens, like your mortgage, are expected, while others may catch you off guard, especially if they’ve been filed without your direct involvement. Here’s a breakdown of the most common lien types and what they mean for sellers.

Voluntary vs. Involuntary Liens

Liens fall into two categories: voluntary and involuntary.

- Voluntary liens are those you agree to, usually in exchange for something of value. The most common example is a mortgage lien, where your lender places a lien on the property until the loan is repaid.

- Involuntary liens are placed without your consent, usually due to unpaid debts. These can include tax, judgment, or HOA liens, among others.

Understanding the difference is key: voluntary liens are expected, but involuntary liens may require urgent attention before you can sell.

Mortgage Liens

A mortgage lien is a voluntary lien placed by your lender when you take out a home loan. The seller must settle the mortgage before transferring the title to the buyer. Most FSBO sellers use sale proceeds to pay off the mortgage at closing. For example, if you owe $200,000 on your mortgage and sell the home for $300,000, $200,000 goes to the lender, and you keep the remaining $100,000 (minus closing costs).

Tax Liens

The government can place a tax lien if you owe back property taxes or income taxes. This lien gives the IRS or local tax authority a legal claim on your property. If you’ve missed several years of property tax payments, your city might file a lien, which you must pay in full or negotiate before selling. Tax liens can delay or complicate a sale if left unresolved.

Mechanic’s Liens (Contractor Liens)

A mechanic’s lien is filed by contractors, subcontractors, or suppliers who haven’t been paid for work done on your home. For instance, they could file a lien if you hired a roofer and didn’t pay the final invoice. Even if you already paid the general contractor, a subcontractor can still file a lien if they weren’t paid. These liens are typical in home improvement situations and can be legally enforced if not addressed.

Judgment Liens

A judgment lien is a result of a court ruling. If someone sues you and wins, they can file a lien to collect on the judgment. Suppose you were sued over unpaid credit card debt and lost the case—the creditor could attach a lien to your property. You must resolve judgment liens through payment or settlement before transferring ownership.

HOA Liens (Homeowners Association Liens)

If your home is part of an HOA and you fall behind on dues, the association can place an HOA lien on your property. This can also happen if you violate HOA rules and don’t pay associated fines. Some HOAs are aggressive about collections, and these liens can proliferate with late fees and legal costs. Before selling, request a payoff statement from your HOA to ensure your account is clear.

Child Support or Alimony Liens

The recipient can file a lien against your property if you owe court-ordered child support or alimony. These are enforceable through family court. For example, if you’re behind on support payments, the state may record a lien that prevents you from selling until the debt is paid. These liens can be complex, so it’s wise to work with an attorney or title company to handle them properly.

How Property Liens Affect FSBO Sellers

Property liens can create serious roadblocks for FSBO sellers. When buyers purchase a home, they expect a clean title—one that’s free of legal claims or unpaid debts. That’s why title companies perform a title search early in the closing process. If a lien is discovered and not adequately resolved, the sale can be delayed, renegotiated, or even canceled entirely.

Here’s how liens can affect your FSBO sale:

- Delays in closing: For example, if a mechanic’s lien from an unpaid contractor is discovered two weeks before closing, the sale may be put on hold until the lien is paid or removed.

- Lost buyer confidence: Buyers may see a lien as a red flag, even if it’s minor. They may worry about legal complications and walk away from the deal.

- Financing issues: If the buyer is using a mortgage, their lender may refuse to fund the purchase if the property has outstanding liens. Lenders require a clean title as collateral for the loan.

Reduced proceeds: As the seller, you may need to pay off the lien before closing, either out of pocket or from the sale proceeds. For instance, if you sell your home for $350,000 with a $10,000 tax lien, that amount will be deducted from your final payout.

Negotiation hurdles: Sometimes buyers will agree to move forward if the seller agrees to resolve the lien quickly or offer a price reduction to compensate for the hassle.

To avoid surprises, it’s smart to run a preliminary title search before listing your home FSBO. Identifying and resolving liens early ensures a smoother selling experience—and helps you maintain buyer trust throughout the process.

How to Check If Your Property Has a Lien

If you’re selling your home without a real estate agent, your property should be lien-free. Liens can delay or derail a sale, so verifying your property's status is a key step in selling.

Check Public Records

Start by searching your local county recorder or clerk's office. Most counties offer online databases where you can search by property address or parcel number to identify any recorded liens. Alternatively, you can visit the office in person to request this information. Some third-party websites also provide access to property records online, though they may charge a fee.

Hire a Title Company

If you prefer professional assistance, consider hiring a title company. These companies conduct comprehensive title searches, uncovering any existing liens or encumbrances. They also offer title insurance, protecting you and the buyer from future claims. While there is a fee for their services, their expertise can provide peace of mind and ensure a smoother transaction.

Work With a Real Estate Attorney

Consulting a real estate attorney is advisable, especially if you discover any liens or a complex title history. An attorney can interpret legal documents, advise on the implications of any liens, and guide you through clearing them. They can also help ensure that all legal requirements are met for a valid and enforceable sale, protecting your interests throughout the transaction.

How to Remove a Property Lien

So, you’ve discovered a few property liens and need them removed to prepare to sell your home. Here’s what you can do.

Pay it Off

The most straightforward way to remove a lien is to pay the debt in full. Once satisfied, the lienholder should provide a "Release of Lien" document. It's essential to file this release with your county recorder's office to clear the lien from public records officially. Without this step, the lien may still appear during a title search, potentially complicating your sale.

Negotiate With the Lienholder

If paying the full amount isn't feasible, consider negotiating with the lienholder. Creditors may accept a reduced lump-sum payment to settle the debt, especially if they believe it increases their chances of recouping funds. Ensure any agreement is documented in writing, and obtain a lien release upon payment.

Dispute an Invalid Lien

If you believe a lien is invalid or was filed in error, you can challenge it. This typically involves filing a lawsuit to "quiet title," which asks the court to remove the lien. You'll need to provide evidence supporting your claim, such as proof of payment or documentation showing the lien was improperly filed. Consulting a real estate attorney can help navigate this process.

Use Escrow to Pay the Lien at Closing

In some cases, you can proceed with the sale by using the proceeds to pay off the lien at closing. An escrow agent will handle the transaction, ensuring the lienholder is paid from the sale funds before you receive any proceeds. This approach allows the sale to move forward while satisfying the lien.

File for Lien Expiration

Liens don't last indefinitely. Each state has statutes of limitations that determine how long a lien remains enforceable. For example, a judgment lien might expire after a certain number of years if not renewed. If a lien has surpassed its legal duration, you can petition the court to have it removed. It's advisable to consult with a real estate attorney to understand your state's specific laws and procedures.

Selling a Property with a Lien: FSBO Strategies

Before you panic about a lien ruining your home sale, take a deep breath—there are still smart, strategic ways to move forward. Let’s explore how FSBO sellers can navigate the process and successfully sell a property with a lien on record.

Disclosing Liens to Buyers

Transparency builds trust. Disclose any existing liens to potential buyers early in the process. Being upfront shows integrity and can prevent legal issues later. Buyers appreciate honesty and are more likely to work with sellers who communicate openly.

Pricing the Property Competitively

A lien can make your property less attractive to buyers. To counter this, price your home competitively. Research similar properties in your area and consider pricing slightly below market value to attract interest. A well-priced home can offset concerns about existing liens.

Offering to Clear the Lien Before Closing

If possible, offer to pay off the lien before closing. This can be done by using the proceeds from the sale to settle the debt. Working with a title company or escrow agent ensures the lien is paid and removed from the title, providing peace of mind to the buyer.

Selling "As-Is" with a Lien

If clearing the lien isn't feasible, consider selling the property "as-is." This approach appeals to investors or buyers willing to take on the responsibility of resolving the lien. Be prepared to adjust the price accordingly and clearly state the terms in your listing to set proper expectations.

Preventing Future Liens on Your Property

As an FSBO seller, keeping your property lien-free is essential for a smooth sale. Liens can complicate or delay transactions, so proactive measures are key.

Stay Current on Financial Obligations

Unpaid debts are a common source of liens. To prevent them:

- Mortgage Payments: Ensure timely payments to avoid default-related liens.

Property Taxes: Pay local, state, and federal taxes promptly to prevent tax liens. - HOA Fees: Keep homeowners association dues current to avoid association-imposed liens.

Manage Contractor Payments Diligently

Home improvements can lead to mechanics' liens if contractors or suppliers aren't paid. To safeguard against this:

- Hire Reputable Professionals: Choose licensed and insured contractors with positive reviews.

Use Joint Checks: When paying, issue checks jointly to contractors and suppliers to ensure funds reach all parties. - Obtain Lien Waivers: Before making final payments, request signed lien waivers confirming all parties have been paid.

- Document Everything: Keep detailed records of contracts, payments, and communications.

Regularly Review Property Records

Mistakes or fraudulent filings can result in unexpected liens. To monitor your property's status:

- Check Public Records: Periodically review your property's records at the county recorder's office or online databases.

- Conduct Title Searches: Before selling, perform a title search to identify any existing liens or encumbrances.

- Consult Professionals: Engage a title company or real estate attorney to assist in reviewing and clearing any issues.

Conclusion

Selling a property with a lien as an FSBO seller may seem daunting, but with the right strategies, it's entirely achievable. By proactively addressing liens—whether by paying them off, negotiating with lienholders, or disclosing them transparently—you can maintain control over your sale and build trust with potential buyers.

By staying informed and taking deliberate steps, you can navigate the complexities of selling a property with a lien and achieve a successful sale.